Posted on September 22, 2017 by Christabelle Harris

Q: what is Personal services income (PSI)?

A: PSI is essentially any income earned from your personal skills or efforts regardless of your business structure (sole trader, partnership, company or trust). If PSI income has been received the relevant rules may apply to you.

If income earned through your business is deemed to be PSI then this income cannot stay in the entity, it must be paid out to the PSI individual as an ‘attributable wage’, in doing so reducing the net profit of the business to nil and preventing any form of income splitting. If the income is not deemed to be PSI the profits can stay within the entity and be taxed accordingly.

Occupations generally affected by the PSI legislation include:

- Builders

- Doctors

- Architects

- Engineers

- Cleaners

- Surveyors

- Consultants

Q: How to work out whether your income is PSI?

A: There are a series of steps in place to determine if these rules apply to you, as listed below.

First, you must determine if more than 50% of the income received from a particular job or contract was for your own services, labour, skills or expertise (as opposed to supply of materials and/or tools and equipment). If so, then all of the income from that job or contract is deemed as being PSI. If not, then the PSI rules do not apply to you.

If you do have PSI income then the below tests must be completed to ascertain whether or not you are running a Personal Services Business (PSB) and therefore allowed to retain the income in your entity:

The Results test – to satisfy the results test the following 3 conditions must be met for at least 75% of the income. If you pass this test the business income derived is not subject to PSI rules:

- You must be paid to produce a specific result or outcome prior to being paid

- You are required to supply the necessary plant & equipment or tools to complete the service

- You are required to fix any mistakes at your own expense or pay someone else to fix them at any time during the contract

If you pass this first test then the PSI rules don’t apply to you. However, if you don’t pass this first test the following Steps are to be continued:

The 80% rule – For this step you must determine how much of the PSI income being tested comes from any one client/contract

- If less than 80%, continue onto step 3

- If more than 80%, PSI rules apply (unless you think you may be eligible for a special determination from the ATO) and any income earned will be attributable to you

If you do not pass the results test but do pass the 80% rule, then you will just need to pass any one of the three additional tests:

- Unrelated clients test: Income received must be from at least two unrelated clients

- Employment test: Do you employ someone who earns at least 20% of the business income?

- Business Premises: Do you have a separate business premises used solely for your business (physically separate from your home and used exclusively for your business).

If you meet one of the above tests the PSI rules do not apply, if not the PSI rules will apply and any income earned will need to put included in your personal Tax Return as an attributable wage.

Share this:

Posted on by Kelsi Keep

Your private health insurance can impact two main items on your Income Tax Return, these include:

- The Private Health Insurance Rebate; and

- The Medicare Levy Surcharge.

The Private Health Insurance Rebate

The Private Health Insurance rebate is an amount that the government contributes towards your private hospital health insurance premiums.

The private health insurance rebate can be received:

- as a premium reduction, which lowers the policy price charged by your insurer; or

- as a refundable tax offset when you lodge your tax return.

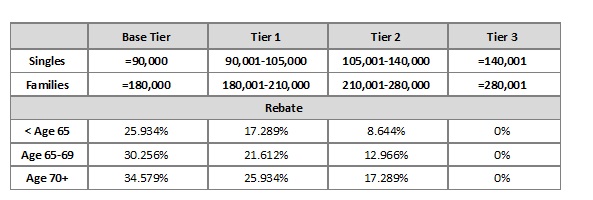

Your entitlement to the rebate is determined based on your income for Medicare Levy Surcharge purposes (discussed later in this article). The table below illustrates the four tiers, the relevant income thresholds for singles and families and the applicable rebate rates.

Note:

- Single parents and couples (including de facto couples) are subject to family tiers

- The thresholds are increased by $1,500 for families with children for each child after the first

- The rebate applies to hospital, general treatment and ambulance policies

- The rebate does not apply to overseas visitors cover

- The rebate percentages above will apply to premiums paid from 1 April 2017 until 31 March 2018.

- In March 2018, the Department of Health will announce the rebate percentages for premiums paid from 1 April 2018 to 31 March 2019

When you lodge your tax return, we will calculate your entitlement to receive a private health insurance rebate.

If you claim your rebate as reduced private health insurance premiums it is important that your Private Health Insurer is aware of which Tier is applicable to you, as this information is not provided to them by the ATO. If you receive more rebate than you are entitled to via reduced private health insurance premiums, the ATO will claim back the excess rebate when you lodge your tax return. This amount will be shown on your tax return as an ‘Excess private health reduction’.

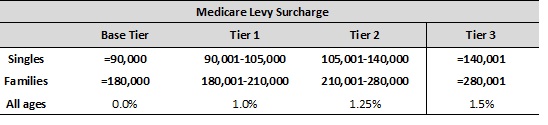

The Medicare Levy Surcharge (MLS)

If you or your family do not have an appropriate level of private hospital insurance cover, and your income for MLS purposes is above a certain threshold, you will be required to pay the MLS. The MLS applies unless you are exempt from paying the Medicare levy as you are a dependant or you satisfy the requirements of one of the following categories:

- Category 1: Medical exemption

- Category 2: Foreign residents exemption

- Category 3: Not entitled to Medicare benefits

The table below details the relevant surcharge amounts based on your income level for MLS purposes.

Note: The rebate percentage is adjusted on 1 April each year.

Your Income for Medicare Levy Surcharge purposes (applicable for calculating the Private Health Insurance Rebate and the Medicare Levy Surcharge) is the sum of:

- your taxable income

- your reportable fringe benefits

- your total net investment losses (including rental property losses)

- your reportable super contributions (including deductible personal super contributions)

If you are between your preservation age and 59 years old, you subtract from the total (above) any taxed element of a super lump sum (other than a death benefit) which you received that does not exceed your low-rate cap.

Your family income for surcharge purposes is the combination of your income and that of your spouse, using the abovementioned criteria.

Share this: